Adding the two variables together, we get an overall variance of $4,800 (Unfavorable). Management should address why the actual labor price is a dollar higher than the standard and why 1,000 more hours are required for production. The same column method can also be applied to variable overhead costs. It is similar to the labor format because the variable overhead is applied based on labor hours in this example.

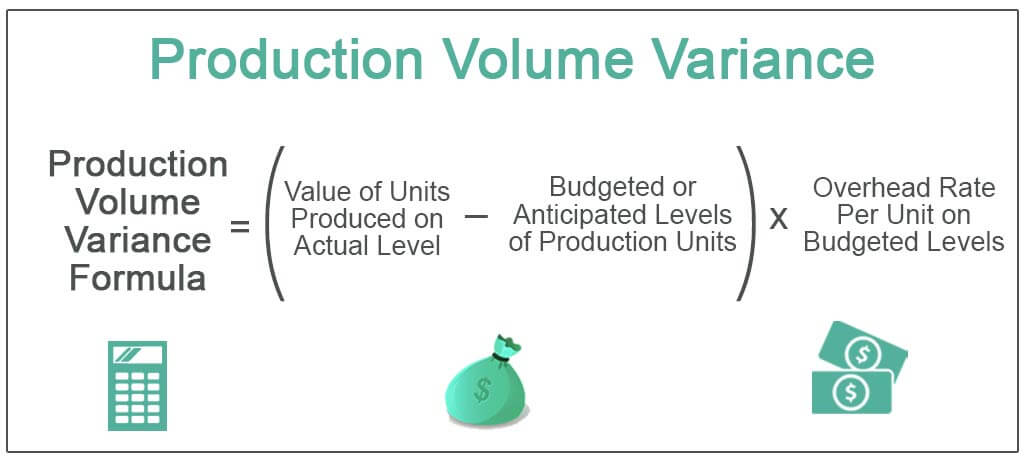

- Fixed overhead, however, includes a volume variance and a budget variance.

- An unfavorable outcome means you used more hours than anticipated to make the actual number of production units.

- Hence, variance arises due to the difference between actual time worked and the total hours that should have been worked.

- If the actual rate of pay per hour is less than the standard rate of pay per hour, the variance will be a favorable variance.

- As mentioned earlier, the cause of one variance might influenceanother variance.

Would you prefer to work with a financial professional remotely or in-person?

Additionally, labor mix variance plays a role, particularly in environments where multiple types of labor are employed. This variance occurs when the proportion of different labor categories used deviates from the standard mix. For example, if a project requires a higher proportion of skilled labor than initially planned, the labor mix variance will reflect this shift, potentially leading to higher costs. Learn how to manage labor variance effectively with insights on components, calculations, influencing factors, and strategies to optimize financial performance. An overview of these two types of labor efficiency variance is given below. Mary’s new hire isn’t doing as well as expected, but what if the opposite had happened?

Variance Analysis

11 Financial’s website is limited to the dissemination of general information pertaining to its advisory services, together with access to additional investment-related information, publications, and links.

Direct labor rate variance

If there is no difference between the standard rate and the actual rate, the outcome will be zero, and no variance exists. The first step in the calculation is determining getting a tax perspective by finding your effective tax rate the labor rate variance. This is achieved by subtracting the standard labor rate from the actual labor rate and then multiplying the result by the actual hours worked.

In this case, the actual rate per hour is $9.50, the standard rate per hour is $8.00, and the actual hours worked per box are 0.10 hours. This is an unfavorable outcome because the actual rate per hour was more than the standard rate per hour. As a result of this unfavorable outcome information, the company may consider using cheaper labor, changing the production process to be more efficient, or increasing prices to cover labor costs. In this case, the actual rate per hour is \(\$9.50\), the standard rate per hour is \(\$8.00\), and the actual hours worked per box are \(0.10\) hours. Standard costs are used to establish theflexible budget for direct labor. The flexible budget is comparedto actual costs, and the difference is shown in the form of twovariances.

Direct labor variance analysis

The reason is that the highly experienced workers can generally be hired only at expensive wage rates. If, on the other hand, less experienced workers are assigned the complex tasks that require higher level of expertise, a favorable labor rate variance may occur. However, these workers may cause the quality issues due to lack of expertise and inflate the firm’s internal failure costs. In order to keep the overall direct labor cost inline with standards while maintaining the output quality, it is much important to assign right tasks to right workers. In this case, two elements are contributing to the unfavorable outcome. Connie’s Candy paid \(\$1.50\) per hour more for labor than expected and used \(0.10\) hours more than expected to make one box of candy.

Calculating labor variance involves a nuanced understanding of both the theoretical and practical aspects of labor cost management. The process begins with establishing standard labor costs, which are derived from historical data, industry benchmarks, and internal performance metrics. These standards serve as a baseline against which actual labor costs are measured.

There are two components to a labor variance, the direct labor rate variance and the direct labor time variance. Figure 10.43 shows the connection between the direct labor rate variance and direct labor time variance to total direct labor variance. In this case, the actual hours worked are 0.05 per box, the standard hours are 0.10 per box, and the standard rate per hour is $8.00. This is a favorable outcome because the actual hours worked were less than the standard hours expected. If the actual hours worked are less than the standard hours at the actual production output level, the variance will be a favorable variance.